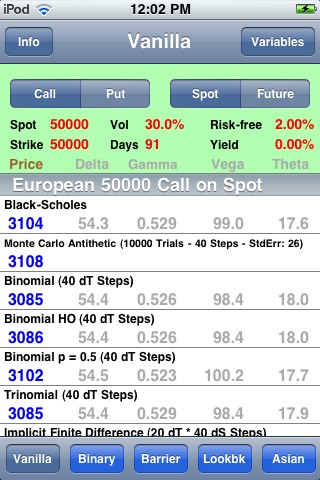

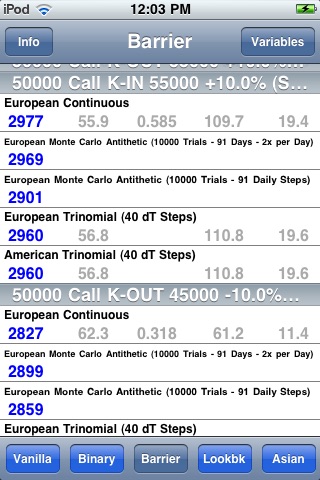

The OPM App provides option pricing across numerous models for the following option types: Vanilla, Binary, Barrier, Lookback and Asian.

Viewing pricing variance across many different models provides a useful reality check.

Please be aware that the exotics may take a minute or two to calculate as will the vanilla options if the steps parameter is set high enough. Each price displayed represents a distinct model so it does take a little time to work through all the calculations.

Dependent upon applicability to the option type, the following pricing models are used:

- Black-Scholes (vanilla) and Black-Scholes type closed-form solutions (others)

- Monte Carlo simulation (trials and samples per day are user-input variables)

- various flavors of binomial and trinomial trees (time steps is a user-input variable)

- finite difference methods (implicit, explicit, and hopscotch - with and without change of variables - time steps and underlying multiplier steps are user-inputs)

- control variate

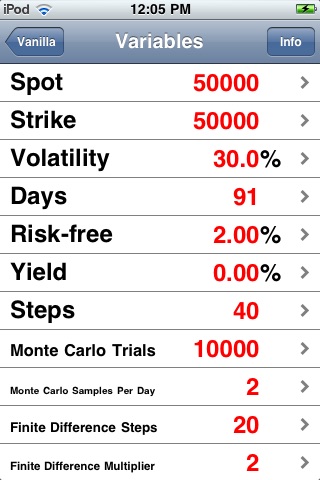

Contract user-input variables are (of course):

1) underlying (spot/future)

2) strike

3) volatility

4) days to expiration

5) risk-free rate

6) underlying yield.

For barrier options, barrier up and barrier down are user-input. Additionally, due to the lack of asian trees recombining, asian time steps are a separate input.